Have Any Question?

Have Any Question? info@mpeslearning.com

info@mpeslearning.com  +44 7452 122728

+44 7452 122728

Back

Back

What is Goodwill in Accounting? Importance, Types, and Examples

Table Of Contents

44 7452 122728

44 7452 122728

11-Feb-2025

11-Feb-2025

Ever noticed how a company’s stock prices decline immediately after a negative event of the brand has caught public eyes? And the word Goodwill is slammed across the news channels. So What is Goodwill in Accounting and how is it quantified? Goodwill is the extra value a business has beyond its physical assets, such as customer loyalty, brand reputation, and strong management. These intangible factors contribute to a company's success but can’t be easily measured. In accounting, goodwill is recorded when a business is acquired for more than the value of its net assets (assets minus liabilities).

For example, if you buy a bakery with a well-known recipe and a loyal customer base, its equipment and building might be worth £300,000, but you pay £400,000 to own the business. The extra £100,000 is goodwill, reflecting the bakery’s reputation, customer trust, and brand value. This makes goodwill an important factor in business acquisitions and financial reporting.

Table of Contents

What is Goodwill in Accounting?

Importance of Goodwill in Accounting

Types of Goodwill

How to Calculate Goodwill in Accounting

Example of Goodwill Calculation

Methods for Goodwill Valuation

Goodwill vs. other Intangible Assets

Benefits of Goodwill in Accounting

Drawbacks of Goodwill in Accounting

Conclusion

What is Goodwill in Accounting?

Goodwill in accounting is an intangible asset that represents the value of a business which is beyond its tangible assets. Goodwill encompasses premium factors such as customer loyalty, brand reputation, workforce expertise, proprietory technology and other intangible elements that contribute to success but that cannot be easily quantified.

Under US GAAP and IFRS Standards, goodwill has an indefinite life and is not amortised. However, it must undergo annual impairment testing to assess any decline in value. Private companies may choose to amortise goodwill over 10 years as an alternative.

Importance of Goodwill in Accounting

Master Financial Accounting And Reporting today!

Goodwill can be positive or negative reflecting the difference between a business’ value and its net assets. Positive goodwill indicates that a company’s market value exceeds its assets and liabilities, while negative goodwill suggests the opposite. This is imperative in valuing a business as goodwill directly impacts the overall brand image for the potential buyers. A high goodwill value often signals a competitive advantage making business appear more attractive to investors and influences strategic decisions. On the contrary, a decline in the goodwill indicates underperformance, poor management choices and puts reliability in question.

From a financial reporting perspective, GAAP and IFRS require goodwill to be recorded annually on the balance sheet as an intangible asset, ensuring transparency in financial statements.

Types of Goodwill

Image explaining Types of Goodwill

Goodwill comes in different forms, depending on the type of business and its customers. At its core, it represents the extra value a business holds beyond its physical assets—things like brand reputation, customer loyalty, and industry standing. But not all goodwill is the same.

There are three broad categories of goodwill in accounting: inherent goodwill and purchased goodwill.

Inherent (or Internally Generated) Goodwill grows naturally over time. It comes from strong customer relationships, excellent service, and a well-established brand. While it adds value, accounting standards don’t allow it to be recorded on financial statements—but it still plays a huge role in a business’s competitive edge.

Purchased Goodwill is the goodwill that appears when one company buys another for more than its net asset value. The extra amount paid reflects intangible benefits like a loyal customer base, market position, and brand recognition. Unlike inherent goodwill, purchased goodwill is recorded as an intangible asset on the balance sheet and must undergo annual impairment testing to ensure its value remains accurate.

Business Goodwill applies to companies that sell products or services. It reflects brand value, market position, and the quality of customer service.

How to Calculate Goodwill in Accounting

Goodwill is calculated when one company acquires another and pays more than the fair market value of its net assets. This excess amount reflects the value of intangible assets such as brand reputation, customer loyalty, and intellectual property.

Goodwill Formula:

Steps to Calculate Goodwill

Determine the Purchase Price

This is the total amount the acquiring company pays for the business.

Assess the Fair Market Value of Assets

Identify the fair value of all tangible and identifiable intangible assets of the acquired company (e.g., property, equipment, patents, trademarks).

Calculate the Liabilities

Include any debts, loans, or outstanding obligations of the acquired company.

Apply the Formula

Subtract the net assets (assets minus liabilities) from the purchase price to determine goodwill.

Example Calculation

A company purchases a café in London for £1.2 million. The café’s assets, including equipment, inventory, and premises, have a fair market value of £900,000, while its liabilities (loans and payables) amount to £200,000.

So, the £500,000 goodwill reflects the café’s brand reputation, strong customer base, and prime location, making it more valuable than just its tangible assets.

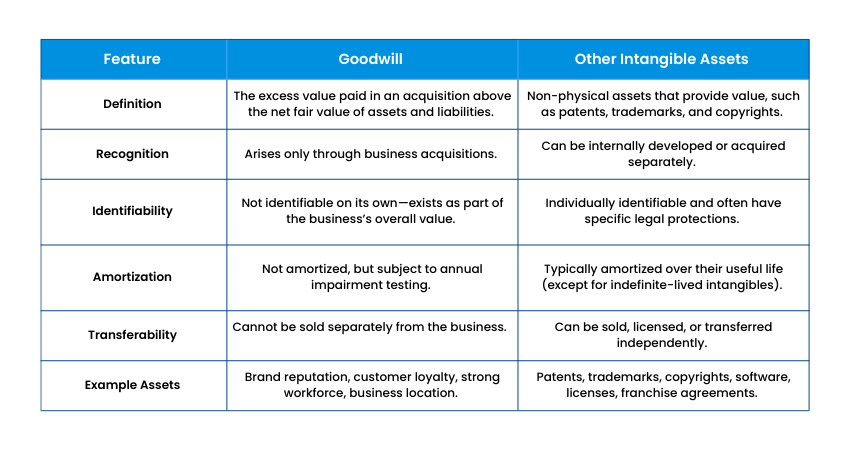

Goodwill vs. other Intangible Assets

Feature | Goodwill | Other Intangible Assets |

Definition | The excess value paid in an acquisition above the net fair value of assets and liabilities. | Non-physical assets that provide value, such as patents, trademarks, and copyrights. |

Recognition | Arises only through business acquisitions. | Can be internally developed or acquired separately. |

Identifiability | Not identifiable on its own—exists as part of the business’s overall value. | Individually identifiable and often have specific legal protections. |

Amortisation | Not amortised, but subject to annual impairment testing. | Typically amortised over their useful life (except for indefinite-lived intangibles). |

Transferability | Cannot be sold separately from the business. | Can be sold, licensed, or transferred independently. |

Example Assets | Brand reputation, customer loyalty, strong workforce, business location. | Patents, trademarks, copyrights, software, licenses, franchise agreements. |

Benefits of Goodwill in Accounting

Goodwill is more than just an intangible asset—it represents a company’s reputation, customer relationships, and brand strength, all of which contribute to its long-term success. While it’s not a physical asset, it plays a crucial role in business valuation, financial reporting, and strategic decision-making.

1. Enhances Business Valuation: A company with high goodwill often commands a higher market value. It reflects brand strength, customer loyalty, and operational efficiency, making the business more attractive to investors and buyers.

2. Strengthens Investor Confidence: Investors consider goodwill as an indicator of a company's stability and long-term growth potential. A company with strong goodwill is perceived as having a competitive advantage and sustained profitability.

3. Facilitates Mergers & Acquisitions (M&A): Goodwill plays a key role in business acquisitions, helping justify premium purchase prices. It reflects intangible value beyond tangible assets, such as customer relationships, brand recognition, and intellectual property.

4. Supports Financial Transparency: Under GAAP and IFRS, goodwill must be recorded on the balance sheet and tested annually for impairment, ensuring accurate financial reporting. Impairment tests help prevent overstated asset values, improving financial accountability.

5. Competitive Advantage in the Market: A business with high goodwill enjoys strong customer retention and brand loyalty, leading to consistent revenue and market leadership. It helps differentiate the company from competitors, making it easier to attract new customers and retain existing ones.

6. Long-Term Business Sustainability: Unlike other assets that depreciate or become obsolete, goodwill has an indefinite life and represents long-term business stability and resilience. Strong goodwill fosters trust with customers, suppliers, and stakeholders, contributing to sustained profitability.

Goodwill is a key financial metric that goes beyond numbers—it reflects the intangible value that makes a company successful. While it doesn't have a physical form, its impact is significant in business growth, investor perception, and overall financial health.

Drawbacks of Goodwill in Accounting

While goodwill is a valuable intangible asset, it also comes with challenges and risks that can impact financial statements and business valuation. Unlike tangible assets, goodwill is difficult to measure, cannot be sold separately, and is subject to impairment losses, making it a complex element in accounting.

Subjectivity in Valuation: Goodwill is difficult to quantify beyond the balance sheet since it represents intangible factors like brand reputation and customer loyalty. The premium paid in an acquisition is reflected as goodwill, but it’s not always clear what specifically justifies this valuation.

2. Cannot Be Sold Separately: Unlike patents, trademarks, or real estate, goodwill cannot be sold or transferred independently. If a business struggles or dissolves, goodwill loses all value.

3. Requires Annual Impairment Testing: Under GAAP and IFRS, goodwill cannot be amortised and must be tested for impairment annually. If goodwill is impaired (its value declines), the company must record a loss, reducing net income and possibly impacting stock prices.

4. Volatility in Financial Statements: Goodwill fluctuates based on market conditions, competition, and financial performance. A sudden drop in goodwill can negatively affect investor confidence and business valuation. Negative goodwill can occur when a company is acquired below its fair market value, indicating financial distress or an urgent sale.

5. Risk of Overpayment in Acquisitions: Companies acquiring businesses with overestimated goodwill may overpay, leading to financial strain and potential write-downs. If the acquired company underperforms, goodwill impairment can lead to significant financial losses.

7. No Direct Economic Benefit: Unlike physical assets (e.g., buildings, equipment), goodwill does not generate revenue on its own. It only holds value if the business continues to perform well and maintains customer loyalty and brand strength.

8. Should Not Be Evaluated in Isolation: Goodwill alone does not provide a complete picture of a company's financial health. It should always be analysed alongside other key performance indicators (KPIs), such as profitability, revenue growth, and market position, to get a well-rounded assessment of business performance.

While goodwill represents intangible business value, it comes with risks that can affect financial stability and investor trust. Companies must carefully assess goodwill during acquisitions, perform regular impairment tests, and avoid overestimating its worth to maintain financial transparency and stability. Additionally, investors and analysts should always evaluate goodwill in conjunction with other financial metrics to gain a more accurate understanding of a company's true value.

Conclusion

Now you have a fair idea of What is Goodwill in Accounting. It reflects a company’s intangible value, including brand reputation, customer loyalty, and market position. While it enhances business valuation and investor confidence, it also carries risks like impairment losses and subjective valuation.